Net Price vs Sticker Price: Why Most Families Pay a Fraction of What the Brochure Says

The $45,000 private-college figure is the number that scares applicants away. The number that matters is about a third of that.

TL;DR: In 2025-26, the average published tuition and fees for a public four-year in-state student is $11,950. The average net tuition and fees, after grant aid, is $2,300 — less than a quarter of the sticker (College Board, Trends in College Pricing and Student Aid 2025). At private nonprofit four-year colleges, the sticker averages $45,000 but the net averages $16,910. The problem is that families eliminate schools based on sticker price without ever running the net-price number that every college is required by federal law to offer. Four free tools, one checklist, ten minutes.

The gap, in the 2025-26 numbers

The College Board’s 2025 Trends in College Pricing report — the annual dataset counselors and policymakers rely on — lays out the two prices side by side.

| Institution type | Published (sticker) tuition & fees 2025-26 | Net tuition & fees 2025-26 |

|---|---|---|

| Public four-year, in-state | $11,950 | ~$2,300 |

| Private nonprofit four-year | $45,000 | ~$16,910 |

| Public four-year, out-of-state | $31,880 | varies by school |

| Public two-year (in-district) | $4,150 | near zero for many Pell-eligible students |

Two pieces of context that rarely make the headlines:

- Sticker prices are rising slower than inflation. Published prices at public institutions increased under 1% in inflation-adjusted terms in 2025-26; private nonprofits rose 1.4% in real terms (College Board Newsroom).

- Net prices are still below their 2012-13 peak. Inflation-adjusted net tuition and fees at public four-years have fallen from $4,450 (in 2025 dollars) in 2012-13 to about $2,300 in 2025-26 — though net tuition did tick up modestly this year (Higher Ed Dive, November 2025).

The sticker-price-as-proxy-for-cost mental model is simply wrong for most students. It is why many applicants and their families never consider schools that could have offered them a cheaper net price than the public flagship.

For counselors, the practical implication is that the “safety/target/reach” framework built on selectivity alone misses half the picture. A private nonprofit that admits 60% of applicants and offers $28,000 in institutional grants to a median-income family is the cheaper option than the in-state public four-year for a surprising number of students. If your shortlist is built on sticker price only, you are leaving money on the table.

Why the two numbers are so different

Net price is not a mystery discount. It is a straightforward subtraction.

Net price = Total cost of attendance − Grant aid

- Total cost of attendance (COA) includes tuition, fees, room and board, books, transportation, and personal expenses.

- Grant aid is money that does not need to be repaid: federal Pell grants, state grants, and institutional grants and scholarships from the college itself.

Critically, net price does not subtract loans or work-study. Those are ways to cover net price, not reductions of it. This is where many financial aid award letters get deceptive — more on that below.

Where does grant aid come from? Three main buckets:

- Federal Pell Grants. The maximum Pell award is $7,395 for 2025-26 and remains $7,395 for 2026-27 (FSA Partner Connect — 2026-27 Pell Grant Dear Colleague Letter). Pell does not need to be repaid. Eligibility is driven by your Student Aid Index (SAI) from the FAFSA.

- State grants. Every state runs its own need-based and merit-based grant programs; amounts and rules vary wildly. California’s Cal Grant, New York’s TAP, and Georgia’s HOPE Scholarship are among the largest.

- Institutional grants. This is the big swing factor at private nonprofits. Endowed colleges routinely discount published tuition by 40-60% for the median admitted student. That is not a scholarship in the merit sense — it is how selective private colleges price their product. The College Board data shows institutional grants are the single largest source of grant aid for students at private nonprofits.

A useful rule of thumb: the more expensive the sticker, the bigger the discount you are likely to get as a middle-income family, because selective privates compete by discounting published price. A $60,000 sticker school may end up cheaper than a $30,000 sticker school for the same student.

The four free tools that compute your real number

Every prospective family should run all four before building a final college list. They take roughly ten minutes each.

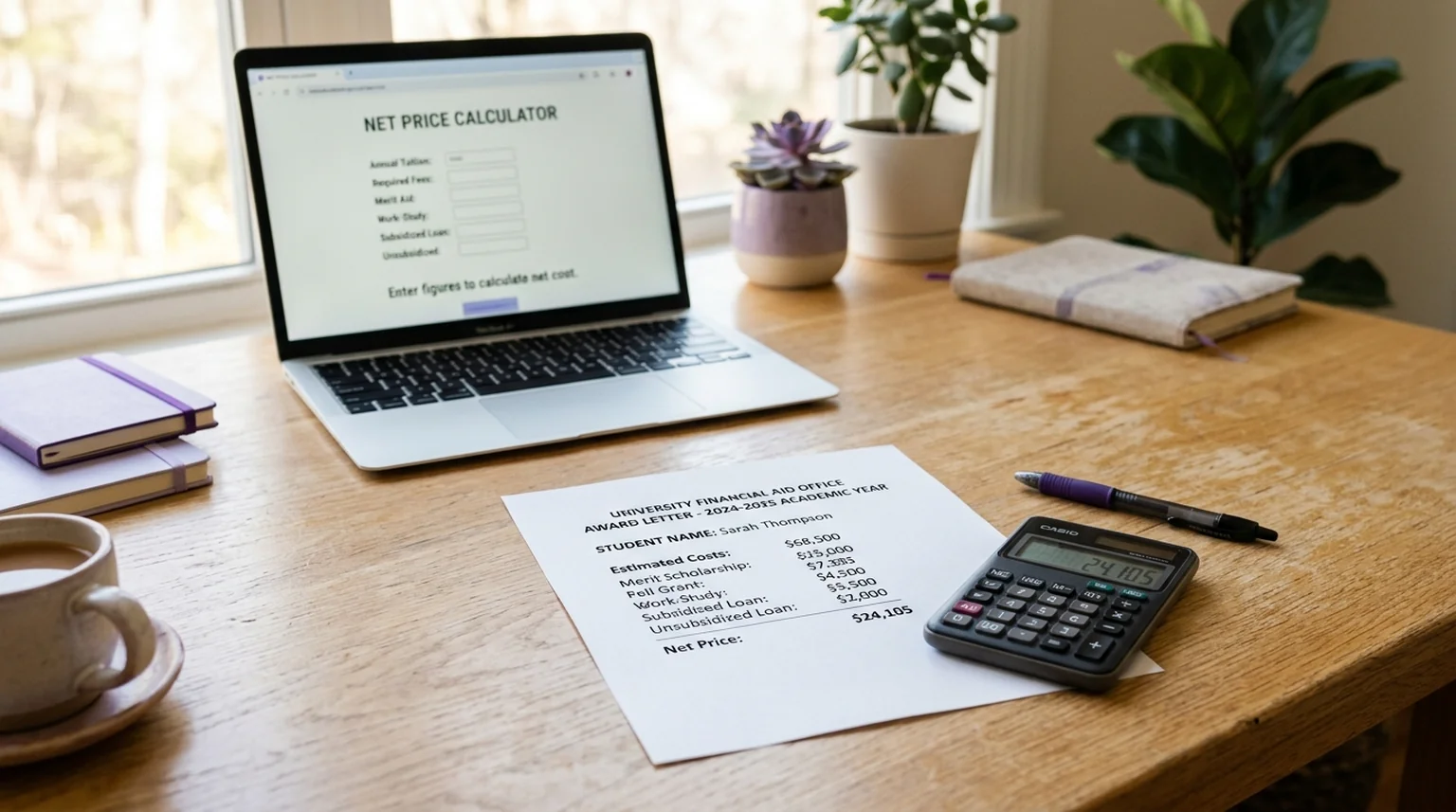

Tool 1: The college’s own Net Price Calculator (NPC)

Federal law requires every college that participates in Title IV programs to post a net price calculator on its website. Go to any college’s “Tuition and Financial Aid” page and look for “Net Price Calculator.” You will enter family income, assets, household size, and a few academic details. It returns an estimated net price personalized to your situation.

- What it is good at: Reflecting the institution’s specific aid policies, including its merit aid tendencies.

- What it is bad at: NPCs vary in quality. Some ask for detailed tax data; others only ask a handful of questions and return rough ranges. Outputs are estimates, not commitments.

- Tip: Run the NPC for every school on the shortlist. The variance across schools for the same family can be $20,000+ per year.

Tool 2: Federal Student Aid Estimator

The Department of Education’s official aid estimator at studentaid.gov returns your estimated Student Aid Index (SAI) — the number that drives how much federal aid (Pell, Direct Loans) you qualify for. It does not tell you how much any specific college will offer; it tells you the federal baseline.

Starting with the 2024-25 FAFSA, the SAI replaced the old Expected Family Contribution (EFC). The SAI can go as low as -$1,500 — a deliberately negative floor intended to identify the lowest-income applicants for targeted aid. On a $7,395 Pell max, an SAI of $0 or less generally means maximum Pell eligibility.

Tool 3: College Scorecard

The Department of Education’s College Scorecard publishes average net price data for every Title IV institution, broken down by family income band ($0-30K, $30K-48K, $48K-75K, $75K-110K, $110K+). It also shows median earnings of graduates 10 years out, median debt at graduation, and completion rates.

- How to use it: Compare net price by income band across three or four schools. You can see instantly whether a school’s median net price for families in your bracket is competitive. Earnings-ten-years-out data puts the price next to the payoff.

Tool 4: NCES College Navigator / IPEDS

The NCES IPEDS Data Center and its consumer-facing site College Navigator report the same average-net-price metric Scorecard uses, sourced from institutional filings. In 2024-25, cost-of-attendance and average net price moved from the Student Financial Aid component to a new Cost (CST) survey component (IPEDS FAQ). The numbers are the same; the reporting architecture changed.

College Navigator is the most accessible interface for comparing schools. Drop in a school name, click “Net Price,” and you get the income-banded table. Do this for every school on your shortlist and the affordability picture clarifies fast.

How to read a financial aid award letter without getting fooled

When you get actual award letters in March and April, the number that looks biggest is often not grant aid. Here is the five-line read:

- Find the Cost of Attendance (COA). It should include tuition, fees, room, board, books, and personal expenses. If the letter only shows tuition, ask for the full COA.

- Identify grants and scholarships. Label anything that does not have to be repaid. Add these up — this is your total grant aid.

- Subtract grants from COA. This is your net price. It is the number that matters.

- Everything else is how you pay the net price. Federal subsidized loans, unsubsidized loans, Parent PLUS loans, work-study, and savings are not reductions of net price. They are payment methods for it.

- Compare net prices, not gross aid packages. A school that offers you $40,000 in “aid” but has a COA of $78,000 is more expensive than a school offering $10,000 in aid but a $25,000 COA.

If an award letter buries loans in the same total as grants, ask the financial aid office for a breakdown. Many schools follow the College Cost Transparency Initiative’s principles to separate grant aid from self-help aid explicitly, but compliance is voluntary and varies.

The 2026 FAFSA landscape, in one section

The FAFSA Simplification Act (passed in December 2020, phased in starting 2024-25) changed several things that matter for your net-price math:

- Questions cut from 108 to 46, with many applicants seeing fewer than 46 thanks to skip logic.

- SAI replaced EFC. SAI can go negative to -$1,500; EFC bottomed at $0.

- IRS direct data import. Applicants must consent to let the IRS transfer tax data directly into the form. Fewer manual tax-number entries, fewer typos.

- Family farm and small-business assets are now reportable for households above certain thresholds, which widened the asset net for some middle-income families.

- Sibling discount gone. Previously, having multiple children in college simultaneously reduced each student’s EFC. The new formula does not divide the SAI across multiple enrolled siblings. This is the most-felt negative change for multi-child households.

Run the FSA Estimator with 2026-27 settings to see what this means for your SAI. If your household has unusual circumstances — a recent job loss, large medical expenses, a one-time capital gain — every financial aid office has a “professional judgment” process to adjust the SAI manually. Ask for it in writing after filing.

Three mistakes that make families overpay

- Eliminating expensive schools based on sticker. A $60,000-sticker Little Ivy with a strong endowment can be cheaper for a median-income family than a $15,000-sticker public regional. Until you run the NPC for both, you do not know.

- Ignoring the COA components beyond tuition. A school with a $12,000 tuition can still cost $28,000 a year once room, board, and books are added. A cheaper-tuition school in a high-cost-of-living city can be the more expensive option all-in. See our guide to picking a college that won’t close for the parallel financial-health check.

- Not comparing net prices across offers. Applicants often commit to the school that “offered the most scholarship” without doing the subtraction. The school offering $28,000 in grants on a $58,000 COA is more expensive than the school offering $12,000 on a $35,000 COA.

The 10-minute net-price worksheet

Do this before you finalize a college list:

- Pick four schools: one public in-state, one public out-of-state, one private nonprofit you like, one reach. (Our best-value rankings are a starting point for the private option.)

- Run each school’s Net Price Calculator (10 minutes total if you have a recent tax return handy).

- Run the Federal Student Aid Estimator once to get your SAI.

- Pull the income-banded average net price from College Scorecard for each school.

- Make a simple table with three columns: school, NPC estimate, Scorecard average for your income band.

- The NPC and Scorecard numbers should be within $2,000-$3,000 of each other. If one school has an NPC estimate far below its Scorecard average, be skeptical — either the NPC is optimistic or the school heavily merit-discounts and you need to confirm merit assumptions.

The output is a ranked list of schools by true expected cost, before a single application essay gets written. It is the single highest-ROI ten-minute exercise in the college search.

For counselors: the two moves that change outcomes

A brief counselor note. Two changes in how you frame affordability tend to move student decisions:

- Show the NPC output in the first meeting. Students who have seen a net-price number for a private nonprofit rarely dismiss those schools on cost alone. Students who have only seen the sticker often do.

- Teach award-letter reading before acceptance season. By the time the letters land in March, emotional commitment is already forming. A 20-minute workshop on “loans are not grants” saves families from expensive defaults.

Our state of higher education guide has the broader enrollment and debt context; this article is the tactical companion.

Sources

- College Board — Trends in College Pricing and Student Aid 2025 — November 2025 — https://research.collegeboard.org/media/pdf/Trends-in-College-Pricing-and-Student-Aid-2025-final_1.pdf

- College Board Newsroom — “Published Tuition Prices at Public Institutions Increase Less Than Inflation” — November 2025 — https://newsroom.collegeboard.org/published-tuition-prices-public-institutions-increase-less-inflation

- NASFAA — “Sticker v. Net Price in 2024-25: The College Board Breaks Down What Students Actually Pay” — 2024 — https://www.nasfaa.org/news-item/34985/Sticker_v_Net_Price_in_2024-25_The_College_Board_Breaks_Down_What_Students_Actually_Pay_to_Attend_College

- Higher Ed Dive — “Net tuition rises at colleges, but costs are far below their peaks” — November 2025 — https://www.highereddive.com/news/net-tuition-2025-college-board/804947/

- Federal Student Aid — Aid Estimator — https://studentaid.gov/aid-estimator

- Federal Student Aid Partners — “2026-27 Federal Pell Grant Maximum and Minimum Award Amounts” — January 2026 — https://fsapartners.ed.gov/knowledge-center/library/dear-colleague-letters/2026-01-30/2026-27-federal-pell-grant-maximum-and-minimum-award-amounts

- U.S. Department of Education — College Scorecard — https://collegescorecard.ed.gov/

- NCES IPEDS — “Average Institutional Net Price FAQs” — https://nces.ed.gov/ipeds/report-your-data/faq-average-net-price

- NCES — College Navigator — https://nces.ed.gov/collegenavigator

- College Board BigFuture — “Focus on College Net Price, Not Sticker Price” — https://bigfuture.collegeboard.org/pay-for-college/get-started/focus-on-net-price-not-sticker-price